McDonald’s declining traffic among lower-income consumers is not happening in isolation. It reflects broader economic pressures that have been building for years.

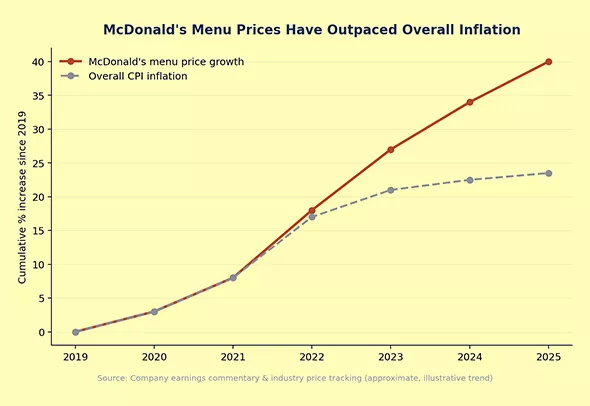

Since 2019, menu prices at McDonald’s have increased by roughly 40% in many markets. While inflation has affected nearly every industry, food-away-from-home costs have risen significantly, making even traditionally affordable fast-food meals more expensive for budget-conscious households.

Recent earnings reports have also revealed a notable shift in customer behavior. Visits from lower-income consumers have declined by double-digit percentages, while traffic from higher-income households has remained stronger and, in some periods, increased by double digits.

This contrast highlights an important economic reality: inflation affects everyone, but it does not affect everyone equally. When the cost of everyday necessities rises faster than income, lower-income households are forced to reduce discretionary spending, while wealthier households often have enough financial flexibility to maintain their lifestyles.

Snapshot

McDonald’s is losing low-income customers because menu prices have jumped roughly 40% since 2019, outpacing wage growth. Combined with record-high rent burdens and rising loan delinquencies among households earning under $45,000, budget-conscious diners simply have less discretionary income making McDonald’s an early indicator of America’s widening wealth divide.

As a result, McDonald’s has become an unexpected case study in the growing wealth divide in America.

What’s Driving Low-Income Customers Away?

1. Prices Have Outpaced Wages

Since 2019, the average McDonald’s menu item price has jumped 40%. Limited-service restaurant prices rose 3.2% year-over-year as of late 2025 outpacing overall inflation at 3%. For lower-income families who spend nearly 30% of their income on food (double the share of higher earners), every price increase hits disproportionately harder.

The Dollar Menu, once the lifeline that reversed McDonald’s fortunes in the early 2000s and grew revenue by 33% is essentially a relic of a different economic era.

2. Housing Costs Are Squeezing Everything Else

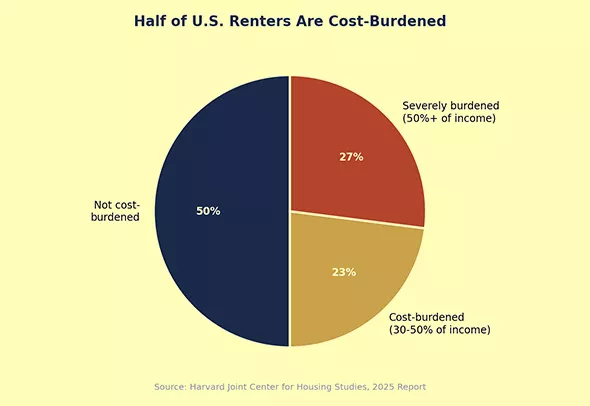

According to a Harvard Joint Center for Housing Studies report, half of all renters in the U.S. 22.6 million people were cost-burdened in 2023, spending more than 30% of their income on housing. Twenty-seven percent were severely burdened, spending over 50% on housing alone. Rents have increased astronomically, and what’s left over for discretionary spending including fast food has fallen to record lows.

Renters earning under $30,000 annually had a median of just $25 left per month after paying for housing and utilities in 2023. That’s not a budget. That’s a crisis.

3. Debt Is Piling Up

Post-pandemic stimulus dried up, and low-income households were hit first. VantageScore data shows that households earning under $45,000 annually have seen “huge year-over-year increases” in 60-day past-due delinquency rates and there has been no dip since 2022. Middle- and high-income households, meanwhile, have largely stabilized.

QUICK TIMELINE: HOW WE GOT HERE

- 2019 – Pre-pandemic baseline. McDonald’s menu prices and household budgets are relatively stable.

- 2020 – COVID-19 – Lockdowns hit low-wage service and hourly workers hardest. Dining rooms close; drive-thru and delivery surge.

- 2020–2021 – Stimulus – Stimulus checks, expanded unemployment benefits, and the Child Tax Credit temporarily boost low-income spending power.

- 2021–2023 – Inflation – Food-away-from-home inflation accelerates; grocery and restaurant prices climb faster than wages for many households.

- 2019–2025 – ~40% Menu Price Increase – McDonald’s cumulative menu price growth reaches roughly 40%, outpacing overall inflation.

- 2023–2026 – Consumers Cut Spending – Savings rates fall, credit card balances climb toward record highs, and lower-income households pull back on discretionary purchases.

- 2024–2026 – McDonald’s Traffic Falls – Earnings reports show double-digit declines in visits from sub-$45K households alongside gains from higher earners.

- Today – A Growing Wealth Divide – The pattern repeats across restaurants, retail, and travel: a bifurcated, “K-shaped” economy.

WHAT’S DRIVING LOW-INCOME CUSTOMERS AWAY?

1. Prices Have Outpaced Wages

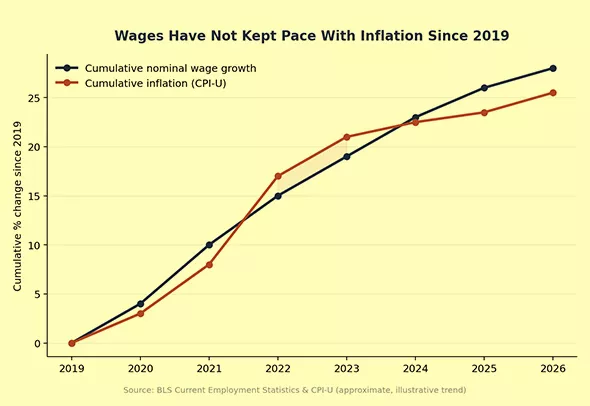

Since 2019, McDonald’s average menu item price has climbed roughly 40%. According to the U.S. Bureau of Labor Statistics, food-away-from-home prices rose 3.5% in the 12 months ending May 2026, while overall consumer prices rose 4.2% over the same period. Restaurant inflation has repeatedly run ahead of wage growth for lower earners over the past several years.

Wage data underscores the gap. Bureau of Labor Statistics data visualized by Statista shows average hourly earnings rose 21.8% from January 2021 to July 2025, while the Consumer Price Index climbed 22.7% over the same stretch leaving real, inflation-adjusted wages down slightly. More recently, the picture has worsened: nominal wages grew 3.7% in the year ending May 2026 while inflation ran at 4.2%, meaning real wages fell roughly half a percentage point.

For lower-income families, who spend a much larger share of their budget on food than higher earners, every price increase hits disproportionately harder. The Dollar Menu, once the lifeline that reversed McDonald’s fortunes in the early 2000s, is essentially a relic of a different economic era.

2. Housing Costs Are Squeezing Everything Else

According to a Harvard Joint Center for Housing Studies report, half of all U.S. renters 22.6 million people were cost-burdened in 2023, spending more than 30% of their income on housing. Twenty-seven percent were severely burdened, spending over 50% on housing alone. Renters earning under $30,000 annually had a median of just $25 left per month after paying for housing and utilities in 2023.

When housing alone consumes half a paycheck, there’s little room left for a $12 combo meal.

3. Debt Is Piling Up as Savings Disappear

Post-pandemic stimulus dried up, and low-income households were hit first. VantageScore data shows households earning under $45,000 annually have seen sizable year-over-year increases in 60-day past-due delinquency rates, with no meaningful dip since 2022. Middle- and high-income households, by contrast, have largely stabilized.

The broader household balance sheet tells a similar story. Americans collectively owed $1.252 trillion in credit card debt at the end of the first quarter of 2026, according to the Federal Reserve Bank of New York a 5.9% year-over-year increase. The personal savings rate fell to roughly 4.0% in early 2026, down from 6.2% in early 2024, as housing costs and inflation eroded household purchasing power. Late-payment delinquency across all household debt climbed to 4.8% a sign that credit is increasingly bridging gaps, not funding extras.

A Two-Track Economy Hidden in Plain Sight

The McDonald’s data is a microcosm of a much larger pattern. Luxury hotels are outperforming budget accommodations. Premium brands are thriving. Affluent consumers are driving an estimated 70% of total consumer spending.

This is what economists call a bifurcated economy two entirely different financial realities operating simultaneously, under the same GDP headline.

To truly understand where you stand in this divide, it helps to benchmark your financial position. Tools like a net worth percentile calculator can give you a concrete sense of how your wealth compares to others across income brackets knowledge that’s increasingly important as the gap widens.

What Is “Wealth” Actually Measuring Here?

It’s easy to conflate income with wealth, but they’re not the same thing. A household earning $60,000 a year with no savings and high debt is in a vastly different position than one earning the same with $50,000 in assets.

Understanding what wealth actually means assets minus liabilities, the ability to sustain your lifestyle without active income reframes the McDonald’s story entirely. Losing customers isn’t just about them spending less. It’s about them having less, full stop.

McDonald’s Response: Too Little, Too Late?

McDonald’s did attempt a course correction. It introduced value meal promotions some reportedly 15% cheaper and leaned heavily into app-based discounts to retain price-sensitive customers. But foot traffic among non-app users still fell approximately 15% year-to-date by mid-2025.

Competitors like Chipotle, Kohl’s, and even pharmacies are reporting similar patterns. The problem isn’t one brand’s pricing strategy. It’s a structural economic shift that no $5 meal deal can solve.

Related Content: How Much Money Does McDonald’s Make a Day?

Why This Should Concern Everyone

Here’s what gets missed in earnings calls and stock analyses: when low-income households pull back, it doesn’t stay contained.

Their spending cuts ripple upward. Restaurants reduce staff. Local economies slow. Tax bases shrink. And eventually, the “two-track economy” becomes a one-track collapse.

The habits that actually build long-term financial resilience matter now more than ever. Research into the most important habits for building wealth consistently points not to income level, but to behavior: consistent saving and long-term investing habits that protect people precisely when economic conditions squeeze spending power.

The Takeaway

McDonald’s losing low-income customers is not a restaurant problem. It is a wealth inequality problem wearing a fast-food uniform.

The data on delinquency rates, rent burdens, menu price increases, and bifurcated spending patterns all points to the same conclusion: the wealth divide in America is not narrowing. It is accelerating. And McDonald’s golden arches are now, inadvertently, a real-time economic indicator of who’s being left behind.

Frequently Asked Questions (FAQs)

McDonald’s is losing low-income customers primarily because of rising menu prices (up 40% since 2019), mounting housing costs that leave families with little discretionary income, and growing debt burdens post-pandemic. The brand that once thrived on affordability has become increasingly unaffordable for its core demographic.

It’s industry-wide. McDonald’s CEO acknowledged that fast-food traffic from low-income households has dropped by double digits across the entire industry not just at McDonald’s. Similar patterns are appearing at grocery chains, discount retailers, and pharmacies.

It signals a growing wealth divide where affluent consumers continue spending while lower-income households cut back sharply. Economists point to stagnant real wages, soaring rent, high delinquency rates among lower-income earners, and the end of pandemic-era stimulus as driving forces.

Start by calculating your actual net worth total assets minus total liabilities and compare it against national benchmarks. Using a net worth percentile calculator is a practical first step to understand where you genuinely fall in today’s economic landscape.

Building financial resilience starts with foundational habits: budgeting consistently, eliminating high-interest debt, and beginning to save and invest even in small amounts. Understanding what wealth really means and adopting the key habits that build it can make a meaningful difference over time, regardless of starting income level.

McDonald’s is losing low-income customers primarily because of rising menu prices (up roughly 40% since 2019), mounting housing costs that leave families with little discretionary income, and growing debt burdens post-pandemic. The brand that once thrived on affordability has become increasingly unaffordable for its core demographic.

It’s industry-wide. McDonald’s own commentary has acknowledged that fast-food traffic from low-income households has dropped by double digits across the entire industry, not just at McDonald’s. Similar patterns are appearing at grocery chains, discount retailers, and pharmacies.

It signals a growing wealth divide where affluent consumers continue spending while lower-income households cut back sharply. Economists point to stagnant real wages, soaring rent, high delinquency rates among lower-income earners, and the end of pandemic-era stimulus as driving forces.

Fast food prices have risen due to a combination of higher labor costs, elevated commodity and packaging prices, and general inflationary pressure across the supply chain. Food-away-from-home prices have consistently outpaced food-at-home (grocery) inflation over the past several years.

It depends on the household. For higher earners, a McDonald’s meal remains a minor, easily absorbed expense. For lower-income households already stretched thin by housing and debt, a $10–$12 combo meal has become a more meaningful budget decision than it was a decade ago.

Higher-income households account for a disproportionate and growing share of total U.S. consumer spending estimated at roughly 70% even though they represent a smaller share of the population. Lower-income households, by contrast, spend a larger share of their budgets on necessities like housing and food, leaving less room for discretionary purchases.